WEM Market Notes/December 2025 — On the Brink: Drivers of the 2026 Outlook in Markets & the Economy

As of December 18, 2025

“If past history was all that is needed to play the game of money, the richest people would be librarians.”

— Warren Buffett

The past year has been the third consecutive year of strong performance across traditional asset classes, especially overseas equity markets, as well as industrial and precious metals. Neither the US tariff-induced sell-off nor the longest US government shutdown on record managed to derail investor optimism. With an ever-rising chorus of complaints, ranging from elevated valuations to high concentration in the best-known market indices flooding major media outlets (not without merit, admittedly), it is worth taking a pause during this holiday season, stepping aside, and reflecting on what may become the key macroeconomic themes of the year ahead.

AI as a Key Growth Driver:

Job Killer or Trigger of a New Supercycle?

AI investment is underpinning productivity and GDP growth, extending well beyond technology into sectors such as energy and infrastructure, although risks of over-enthusiasm and higher volatility remain.

When mechanical weaving machines were introduced at the start of the 19th century, they were followed by the Luddite movement, which sought to halt their rollout in English factories — often by force. History shows how that ended. The resulting surge in productivity that reshaped the textile industry and many others may serve as a blueprint for what artificial intelligence could mean for 21st-century economies. Some argue that the “silent revolution” driven by AI-enabled productivity gains could become the engine of the next long-term macroeconomic supercycle — the so-called Kondratieff wave.

AI is transforming not only the technology sector, where it is driving unprecedented demand for semiconductors, data management, fintech solutions, and cybersecurity. While productivity gains and higher corporate profits remain the dominant expectations, the unintended consequences of rapid AI adoption include labor-market disruptions and the potential formation of asset bubbles. Overseas, an uptick in productivity growth has already been observed. The AI sector was a key driver of economic growth in 2025, particularly in the US and Asia, although concerns about sustainability emerged toward year-end. Nevertheless, continued sector expansion may unlock new growth opportunities, encouraging companies to step up investment and providing fresh impetus to both private and public consumption.

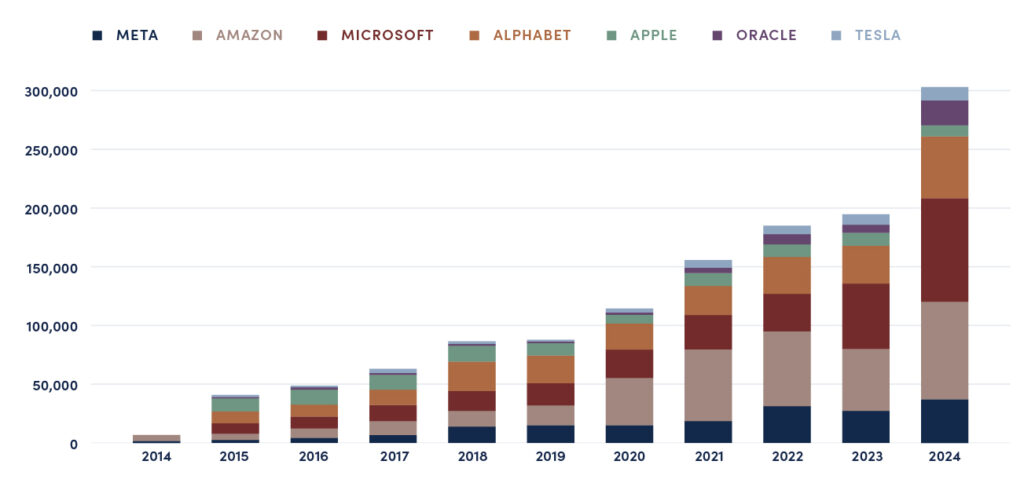

Capital Investments

Source: Bloomberg Professional Terminal. Data as of 17.12.2025.

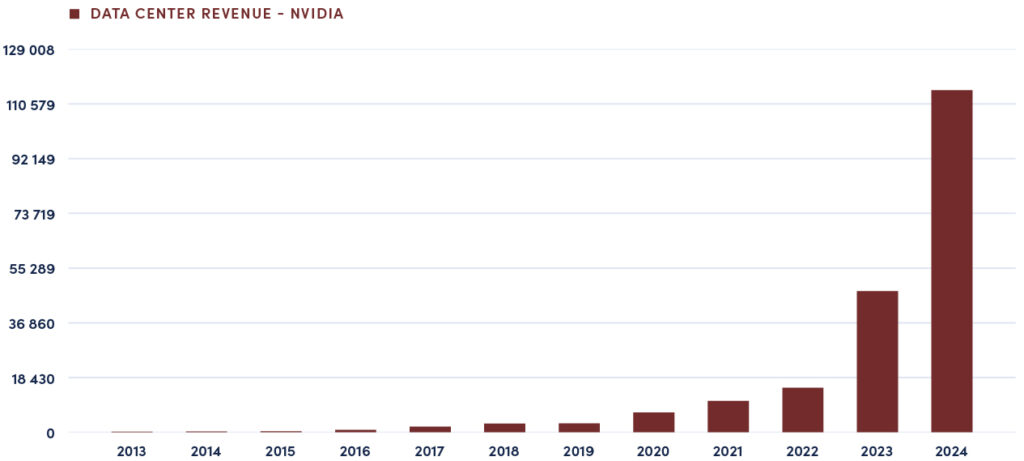

NVIDIA Data Center Revenues

Source: Bloomberg Professional Terminal. Data as of 17.12.2025.

Tariffs and Trade Fragmentation:

The End of Globalization?

Potential inflationary shocks and growth headwinds from US tariffs have been mitigated by carve-outs and supply-chain resilience, while a broader shift toward economic security is underway.

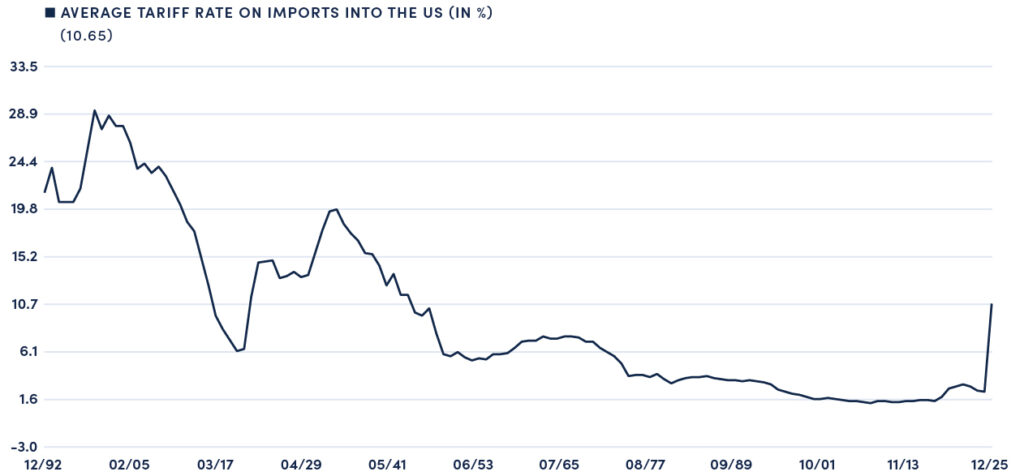

The trade war initiated by the new US administration has lifted the effective tariff rate on US imports to its highest level since the 1930s. That era coincided with the Great Depression, which was preceded by a decade of similar protectionist policies under Republican presidents Warren Harding, Calvin Coolidge, and Herbert Hoover.

US tariff policy is significantly reshaping global trade flows by incentivizing companies to prioritize supply-chain resilience, leading to a strategic shift toward shorter, more reliable networks (nearshoring and friend-shoring). These policies have also ignited re-industrialization efforts in Europe, led by Germany, where fiscal stimulus now rivals the scale seen after reunification. Despite these structural changes, the initial impact of tariffs on global trade, inflation, and spending has been less severe than initially expected. On the one hand, the most protectionist trade stance in 80 years has raised concerns about softer US growth entering 2026. On the other hand, 2025 demonstrated that countervailing forces — AI-related investment, productivity gains, and capital inflows — can meaningfully mitigate

the overall impact.

Average Tariff Rate on Imports to the USA

Source: Bloomberg Professional Terminal. Data as of 17.12.2025.

Fiscal Stimulus and Rising Debt Concerns

Policies such as the US OBBBA and German extra-budgetary investment funds support growth but raise questions around long-term debt sustainability.

Tax cuts introduced under the OBBBA (One Big Beautiful Bill Act) could add up to USD 3.4 trillion to US public-finance deficits over the next decade. The interaction between US tax policy, the allocation of tariff revenues, and deregulation will shape the investment environment overseas. At the same time, elevated budget deficits and rising sovereign debt increase the likelihood of persistently higher inflation. While inflation tends to boost nominal tax revenues, it also helps reduce the real debt burden. Front-loaded US fiscal policy could therefore deliver growth benefits materializing in 2026 – 2027.

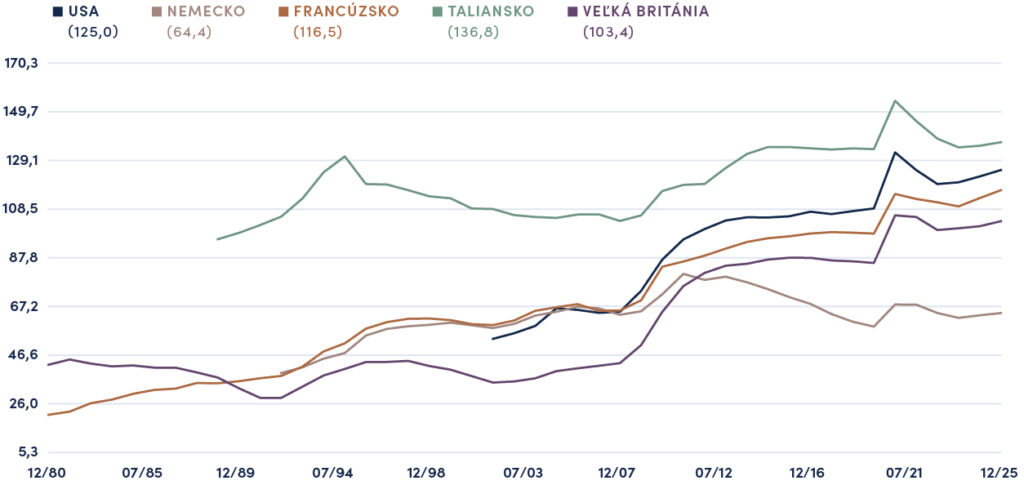

That said, many developed economies are already grappling with high public-debt levels. An increasing number are pushing the boundaries of what is considered sustainable: among advanced markets, Japan, Italy, the US, France, Canada, the UK, and Spain all carry public debt at or above 100% of GDP. Fiscal spending continues to support growth, but in many countries — particularly those with aging populations — government expenditure is already at “escape velocity,” set to rise further as a share of GDP unless decisive structural reforms are implemented.

Germany announced an unprecedented stimulus package in late 2024, planning to increase total public spending by 2.2% of GDP by 2027 and to allocate approximately €500 billion toward infrastructure modernization. An analytical report by Mario Draghi, published in autumn 2024 and later forming the basis of the European Commission’s memorandum titled “Competitiveness Compass”, called for massive additional investment in energy, infrastructure, and the EU’s overall competitiveness.

Level of Public Debt

Source: Bloomberg Professional Terminal. Data as of 17.12.2025.

Labor-Market Softening and Demographic Challenges:

Set to Persist

Softening labor conditions in the US and globally are already shaping policy responses, even before AI-related job displacement fully materializes.

After two consecutive years of monetary easing, the labor market is likely to be the key determinant of the pace and scale of further Federal Reserve easing in 2026, provided inflation remains contained. Should labor-market weakness persist — driven by immigration restrictions, federal layoffs, and labor-saving AI technologies — additional Fed rate cuts could become feasible.

AI may exert a more visible impact on employment, particularly for software-as-a-service providers and other technology firms. Nonetheless, inflation and labor-market conditions are broadly expected to stabilize. The Federal Reserve frames its policy outlook through the Phillips-curve relationship, which links wage inflation to unemployment. As labor-market slack increases, the Fed sees downside risks to inflation. The final weeks of the year saw a marked deterioration in US labor-market indicators. Historically, once labor-market conditions begin to weaken, the trend tends to persist and often intensifies over time. As a result, labor conditions are likely to remain soft amid reduced labor supply and cautious hiring behavior.

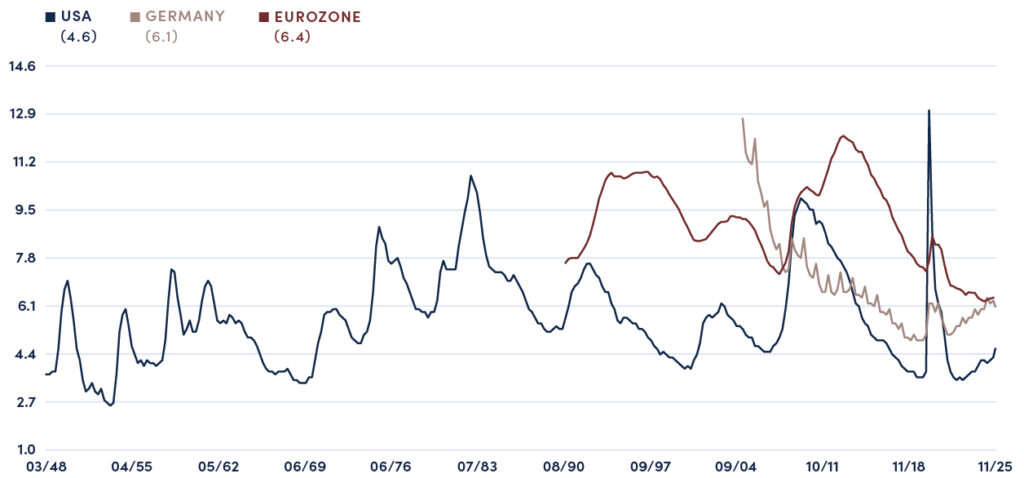

Unemployment Rate

Source: Bloomberg Professional Terminal. Data as of 17.12.2025.

Energy Transition and Grid Infrastructure:

The Next Major Capex Cycle

AI-driven electricity demand is accelerating investment in renewables and power-distribution networks.

Electricity demand from data centers is expected to grow by more than 150% by 2030. The boom in data centers — driven partly by AI and partly by non-AI technological growth — will catalyze a generational increase in global power demand over the coming years. The most binding constraint on AI expansion increasingly appears to be the availability of affordable electricity. In the US, utilities face an estimated five-year backlog in adding new generation capacity and connecting it to the grid. Roughly 70% of regional power markets are already operating near capacity, with demand set to rise sharply through the end of the decade.

As a result, infrastructure linked to data-center expansion is positioned for sustained growth, supported by continued investment in generation capacity and extensive grid upgrades — particularly for renewable energy and EV-charging infrastructure. If these scenarios unfold, they are also bullish for industrial metals such as copper and aluminum, which are directly exposed to energy-transition dynamics and AI-driven data-center demand, while remaining highly sensitive to any rebound in global growth.

Rapid AI adoption is already pushing US electricity demand higher. By 2030, data centers are projected to add power demand equivalent to Sweden’s current annual electricity consumption. By 2035, they could account for up to 9% of total US electricity usage. Consequently, the AI boom is likely to place upward pressure on electricity prices. Although electricity represents less than 3% of the CPI basket, it remains a critical input cost for manufacturers, retailers, and service providers.

For more information, please contact your Wealth Manager.

Chief Economist